The Retiring FITT® System

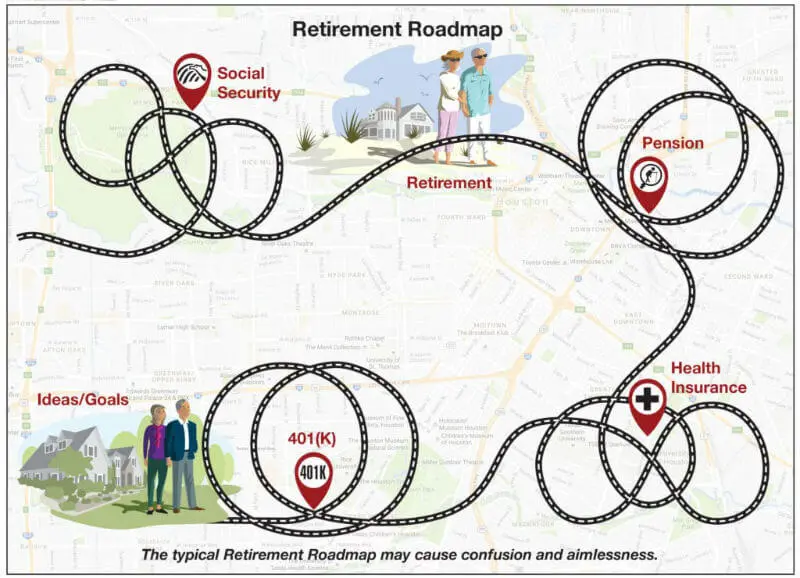

A Typical Approach

Years ago, Lisa was on the phone with HR. They were telling her that she needed to complete her pension form and send it in, so her pension checks could start coming 3 months from now.

HR offered to answer any more questions she may have, but the answer to most of the questions was that they weren't able to offer individual advice.

Lisa and Mark had been to a number of financial seminars, only to discover that the presenter had products to sell and wasn't answering Lisa and Mark's specific questions.

It was like having a complicated medical condition and no doctor to put everything together into a solid care plan – just partial plans from several doctors and having to put it all together as the patient.

The Internet and their co-workers offered some good information but also a lot of conflicting and confusing information.

One important piece of information they discovered was that some of the choices that they had to make could not be changed once made.

- If they made a paperwork mistake, certain mistakes could not be corrected.

- If they made a bad choice because they didn't understand the details, certain choices could not be altered.

- If they relied on bad advice from someone, even if the advice came from a "professional," certain decisions could not be corrected, and others could only be corrected by paying high penalties.

Mark and Lisa discovered that it was important to make good decisions because whatever they decided would affect their finances for the rest of their lives – good or bad.

Lisa was crying in our conference room as she told their story. She was right – people need one place to go and get all of their questions answered and answered correctly. They need a way to build a thorough plan that addresses all of their concerns, not just some of them.

Selah's Retiring FITT® System for achieving Financial Independence Today ~ Tomorrow® was the result of Lisa's tears and years of innovative work.

The Typical Approach Isn't Always Enough

It is certainly possible to retire using the typical approach – start with a financial advisor with a good personality and have them do a complimentary financial plan for you. Then, you decide whether or not to use their services for the investing and/or annuity or insurance products that they recommend.

Then, use a combination of other salespeople or professionals to address the remaining concerns: taxes, Social Security, health care insurance, long-term care insurance, estate planning, and maybe more.

Sometimes that's just not good enough.

Many complimentary financial plans take fewer than 10 minutes to complete. Many risk assessments are done by asking just a few questions. Tax planning often involves a quick conversation, even when math makes more sense.

The typical complimentary financial plan makes a lot of sense when detailed planning is not needed, assuming reasonable projections for inflation, market returns, and tax rates are used.

The typical complimentary financial plan makes sense, in the same way that a Telemedicine visit makes good sense for a handful of common conditions.

But if your financial situation is more complex and needs detailed planning to make sure all of the pieces fit together well and work in your best interest, then a typical financial plan might not be what you need.

The Retiring FITT® System is hours of in-depth, advanced planning, not 10-minute planning.

Here Are Just a Few of the Differences…

A TYPICAL FINANCIAL PLAN |

RETIRING FITT® SYSTEM |

|

|---|---|---|

| Risk | Determined by asking a few questions or through general conversation. | Risk level is determined from 4 different perspectives: emotional, mathematical, behavioral, and temporal. |

| Market Volatility | Average market performance is assumed year after year. | Market volatility is tested through a series of simulations. |

| Scenarios | Each plan is one scenario. | Multiple scenarios are used for many different reasons, such as life changes, tax planning, finding your spending guard rails, considering the consequences of different decisions, and more. |

| Specific Planning Items (Taxes, Pensions, Social Security, Deferred Comp, Medical Insurance/Costs, Inheritance, etc.) | One assumption is used throughout the plan. | Different options and strategies are compared mathematically, and sensitivities are identified in order to facilitate informed decision-making. |

What's Next for You?

The process of retiring has become mind-numbingly complex. It leaves many feeling scared, overwhelmed, and confused.

It challenges very successful executives, professionals, and business owners, and for good reason.

When you retire, you must make several irrevocable decisions, so you want to make the smartest informed decisions after carefully considering your options.

Having a systematic and established process for making retirement decisions and putting a plan in place can help reduce people's feelings of being scared, overwhelmed, and confused. That's why the Retiring FITT® System was created.

If you prefer a confidential way to get your retirement questions answered, schedule a 57-minute Retiring FITT® Conversation. It's 57 minutes focused on YOU, your retirement, and your future. No pressure. No obligation. Just honest answers to all your questions about retiring well.

Let us help you Retire FITT® and achieve Financial Independence Today ~Tomorrow®.

The preceding is a hypothetical case and is for illustrative purposes only. Actual performance and results will vary. Any resemblance to actual people or situations is purely coincidental. This story does not constitute a recommendation as to the suitability of any investment for any person or persons having circumstances similar to those portrayed, and a financial advisor should be consulted.